The Key Contributors to Corporate Fraud and How to Mitigate Risk

Fraud is pervasive in all aspects of our personal and professional lives. Aside from the Nigerian Prince email where he needs your personal help to transfer large amounts of money out of his home country and into your bank account, corporate fraud is on the rise in the United States. Harney provides forensic accounting and fraud examination.

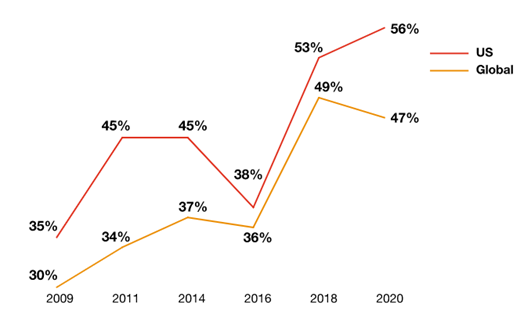

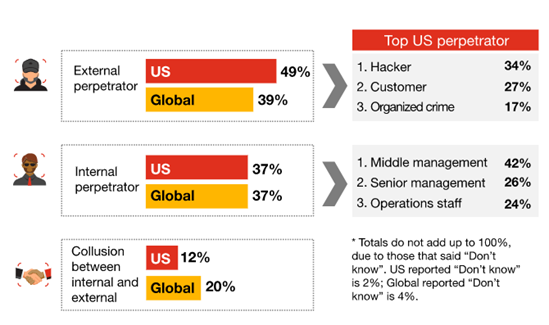

In PwC’s 2020 Global Economic Crime and Fraud Survey, it indicated a record-high 56% of domestic companies had experienced fraud in the past 24 months, with customer fraud, cybercrime and accounting fraud being more reported. Approximately 50% of these reported frauds involved internal company employees at all levels of responsibility,

Key Factors Contributing to the Rise of Fraud

- Identifying and proving fraud is difficult. Because records will likely be unavailable or incomplete, forensic investigators must have a keen eye to be able to identify deceptive financial activity. In many cases, the signs for fraud are not obvious and the paper trail is limited. It is critical to spot common red-flags signs of internal fraud schemes. But the first step is knowing where to look.

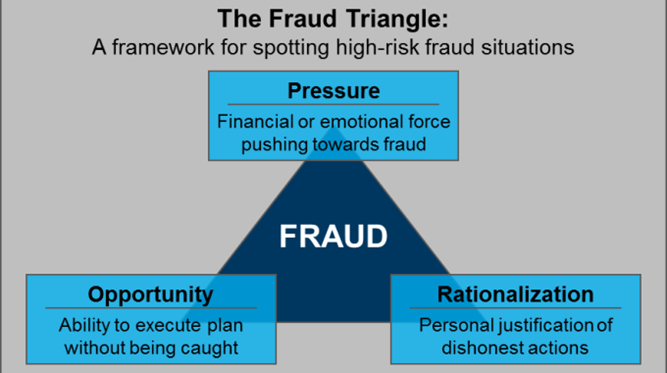

- The Cressey “fraud triangle.” Individuals who perpetrate fraud possess opportunity, rationalization and pressure — three essentials for the crime to occur. When an individual with high-level or unmonitored access to monies begins to rationalize his actions against perceived financial hardship, entitlement or the belief that he can act without detection or punishment, conditions are ripe for fraud.

- Bankruptcy fraud is commonplace. According to Credit Infocenter, Bankruptcy fraud is a form of white-collar crime that usually involves at least the three distinct activities listed below. These behaviors are not a surprise to those who regularly practice in bankruptcy court.

- Concealment of assets

- Intentionally filing incomplete or false forms

- Filing multiple times using false or real information in multiple jurisdictions

- Bankruptcy fraud is not frequently prosecuted. According to annual statistics from the U.S. Department of Justice covering multiple years, it is not uncommon for less than 1% of criminal referrals to result in an actual prosecution. Federal prosecutors will take a slam-dunk case, which are few and far between. For a case to get to court, it must meet certain fiscal or high-profile criteria. The five most-common allegations are:

- Tax fraud

- False oath or statement

- Concealment of assets

- Bankruptcy fraud scheme

- Identity theft or use of false/multiple Social Security Numbers

Here’s a recent example of a successful prosecution.

The United States Attorney’s Office for the Southern District of New York announced on February 3, 2021 that Daniel Kamensky, the founder and manager of New York-based hedge fund Marble Ridge Capital, pled guilty to one count of bankruptcy fraud in connection with his scheme to pressure a rival bidder to abandon its higher bid for assets in connection with Neiman Marcus’s bankruptcy proceedings so that Marble Ridge could obtain those assets for a lower price.

U.S. Attorney Audrey Strauss said: “Daniel Kamensky abused his position as a committee member in the Neiman Marcus Bankruptcy to corrupt the process for distributing assets and take extra profits for himself and his hedge fund. Kamensky predicted in his own words to a colleague: “Do you understand…I can go to jail?”… “this is going to the U.S. Attorney’s Office.” A complete copy of the full Sealed Complaint can be found here.

Will These Conditions Worsen Or Improve? And If Fraud Is Indeed On The Rise, What Can Be Done About It?

It is reasonable to believe that virtual working arrangements by many employees over the past year in response to the COVID pandemic will challenge companies to maintain robust controls and security procedures. At the same time, auditors and regulators struggle to achieve the requisite level of onsite and in-person examinations that are key to both deterrence and detection. This confluence of events might be setting the stage for an unprecedented tsunami of post-pandemic fraud discoveries. As a result, management must take decisive and proactive action.

Here Are 4 Key Steps for Preventing Fraud:

1. Learn To Recognize Those At Higher Risk

Study the warning signs to enable early identification of common perpetrators of fraud. They are often long-time employees, well-liked and trusted. Worse, they may also be a relative or close childhood friend or company principal(s).

According to a prior Association of Certified Fraud Examiners’ (ACFE) Global Fraud Study:

- Fraud will originate primarily within accounting, operations, sales, upper management, customer service, purchasing and finance departments. In fact, the data revealed that more occupational frauds originated in the accounting department (16.6%) than in any other business unit.

- The higher the perpetrator’s authority, the greater the losses will be. For example, the median loss in a scheme committed by an owner/executive was $703,000. This was more than four times higher than the median loss caused by managers ($173,000) and nearly 11 times higher than the loss caused by employees ($65,000).

- The more individuals involved in an occupational fraud scheme, the higher losses tended to be.

- Male fraudsters outnumbered females by a 2 to 1 ratio.

Surprisingly, some of the most trusted employees are the ones that end up committing fraud. In many cases, these professionals have a limited segregation of duties, are often given many responsibilities and trusted with so much, allowing them opportunities to commit fraud and conceal it effectively.

For example, a woman who owned a home construction company had her best, most trusted friend work for her in the accounting department. She had authority to issue checks, sign checks, record the checks and reconcile the bank accounts. She stole two million dollars from her “dearest” friend.

2. Recruit And Retain More Competent, Ethical Talent

Make a conscious effort to recruit talent with a strong set of ethics and consider having your candidates perform an ethics test before hiring them.

- Perform background checks on all employees and be sure you check for more than just criminal records.

- Look for warning signs: Does the employee have bank liens, prior bankruptcy filings or other such anomalies that may demonstrate a potential financial hardship and incentive for the employee to steal?

- Establish written rules of ethics and ensure that all employees receive mandatory training on an annual basis. Also, revisit these standards each year to promote compliance.

3. Increase Anti-Fraud Controls In Your Business

ACFE surveys consistently demonstrate that the organizations which implement common anti-fraud controls — including job rotation, surprise audits, risk assessments, fraud training, codes of conduct, etc., experience considerably lower losses and time-to-detection than organizations lacking these practices. In addition, setting up a whistleblower hotline is a small investment that can bring to light all sorts of unethical behavior if the leads are followed appropriately.

For example, one of our former clients implemented an ethics policy, training and hotline within their organization. This resulted in a whistleblower tip that led to extensive allegations of kickbacks and false billings. Our clients’ efforts not only promoted fraud awareness and intolerance, the hotline helped uncover rampant unethical behavior among several employees.

To optimize timely prevention or detection of fraud, it’s important to establish rigorous governance processes, create and reiterate visible anti-fraud culture, establish regular risk-assessment procedures, and take swift action in response to fraud allegations, including actions against those involved.

For example, a large school district we worked with performed a fraud risk assessment in one of its departments and discovered several control weaknesses. It implemented new controls and a few months later, because of these new controls, discovered a large embezzlement scheme resulting in the firing of an employee and identification of the loss of hundreds of thousands of dollars.

4. Establish Tone At The Top

Establish clear tone, from the Board and C-level down, that your organization will not tolerate fraud. Perception is reality: When management and staff have been reminded of your zero tolerance policies, they will follow your lead.

By way of negative example, we worked for a Fortune 500 organization that performed an audit of employee expenses, resulting in the identification of significant waste and abuse at the director level. We discovered that photo editing software was being used to change amounts and details of receipts and the fraudsters submitted the same receipt for multiple expense reports. When brought to the attention of management, we were told the directors were “off limits.” This is an example of poor “tone at the top.”

Bringing It All Together

Fraud risks are higher than ever due to increasing technology access, lack of proper internal controls, recent modifications to normal business practices required because of COVID and other fraud detection challenges. With ongoing diligence and awareness, you can effectively identify the warning signs and reduce fraudulent behavior before it negatively impacts your organization.

And it never hurts to ask for help. Enlisting a consultant can help you to effectively detect fraud and other suspicious activity before it is too late. With our forensic accounting and fraud examination, Harney Partners leverages forensic data analytics, a proven methodology that assists in identifying the highest risks of fraud, abuse and waste. Contact us today to schedule your free consultation.